[ad_1]

This is a segment from the 0xResearch newsletter. To read full editions, subscribe.

Banks take in deposits to invest a portion in riskier, illiquid assets — that’s how they make money.

This “borrow short, lend long” business model is otherwise known as fractional reserve banking. As long as not every depositor wants their money at once, everyone’s happy!

When crisis mode hits and users rush for the exits, the risk models of banks are put to the test.

At the heart of the problem is non-transparency around a bank’s liabilities and available assets. You could theoretically avoid this problem if that information was visible, as you could curate your own risk models.

Enter infiniFi, a new DeFi protocol on Ethereum that aims to replicate the entire stack of fractional reserve banking onchain.

How it works:

- Users deposit stablecoins for iUSD receipt stablecoin.

- For lower risk yield, stake iUSD for siUSD. This is liquid.

- For higher risk yield, lock up iUSD for liUSD. This is illiquid.

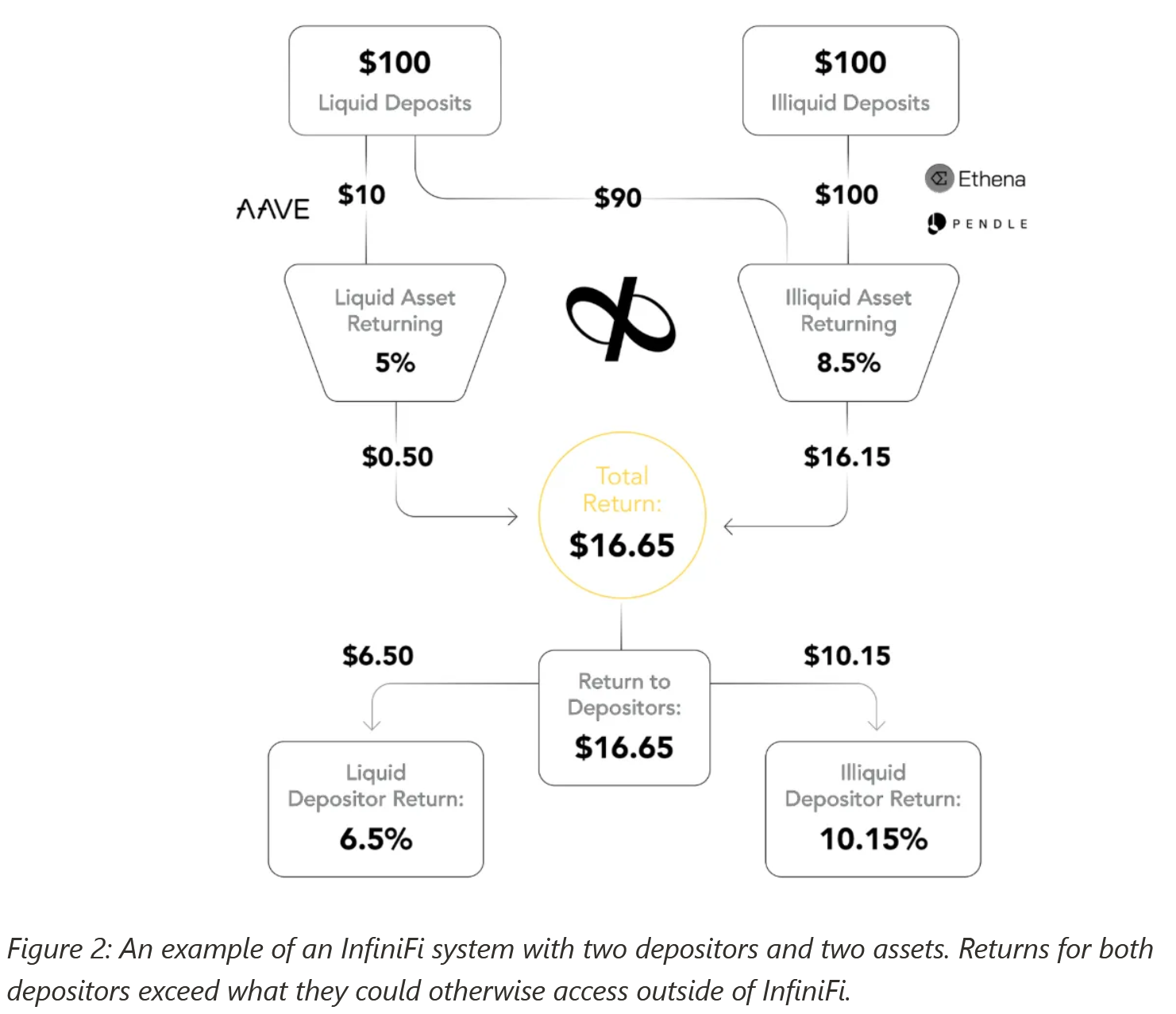

Now the “fractional reserve banking” component comes in.

InfiniFi deploys the liUSD liquid tranche capital into lower risk return money markets like Aave or Fluid, while optionally deploying the siUSD illiquid tranche into higher risk return strategies. (Governance will eventually determine these decisions.)

That exact ratio is informed by the demonstrated preferences of depositors and which yield options they select (siUSD vs liUSD).

The positive-sum outcome? InfiniFi gets to distribute amplified yields for both groups of depositors than if they had pursued their strategies individually.

Source: infiniFi

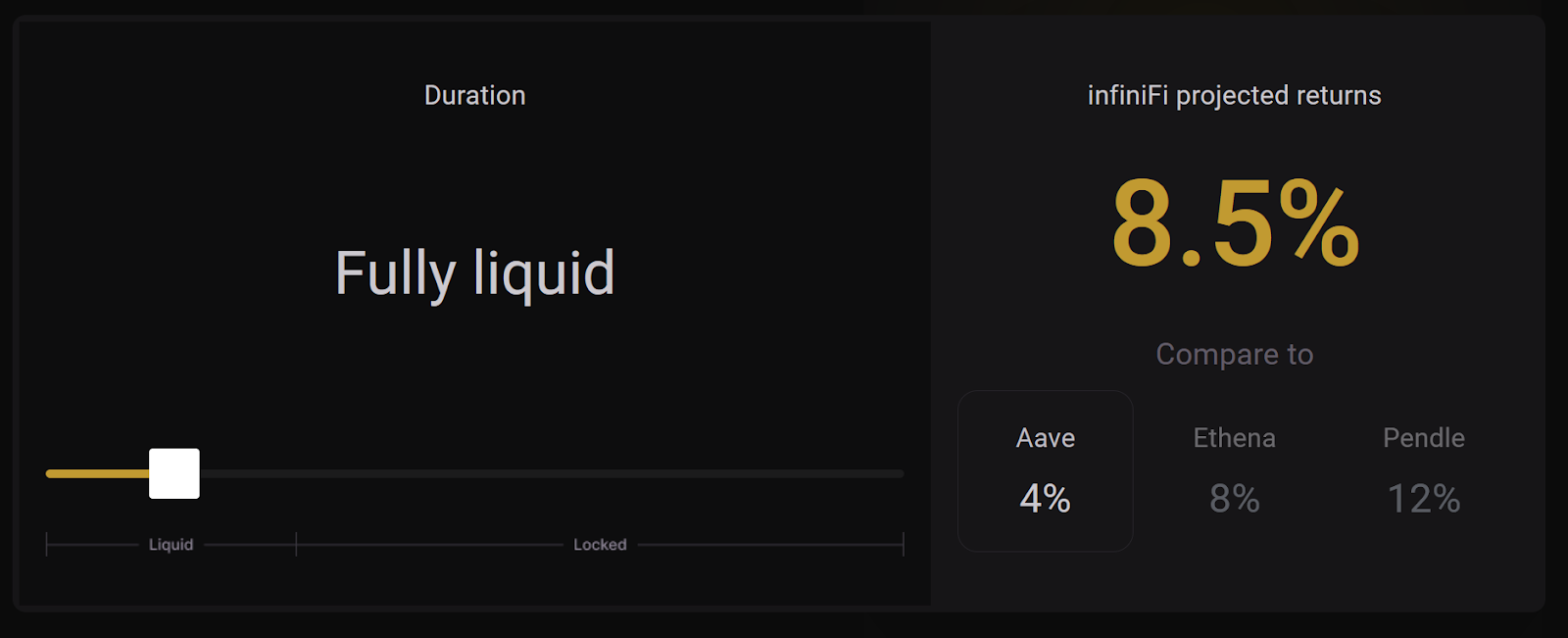

Based on infiniFi’s website, whether you’re opting for a liquid (siUSD) or locked (liUSD) yield, you get a comparatively superior yield than the underlying protocol.

Source: infiniFi.

Source: infiniFi.

It’s a neat business model.

But what infiniFi is doing in itself — borrowing short and lending long — isn’t all that different from what banks usually do.

The innovation comes from the fact that the entire stack is on the blockchain.

That’s how you, as a user, can sleep easily at night — you know your bank isn’t pulling a Sam Bankman-Fried and pursuing unchecked leverage against the most illiquid assets.

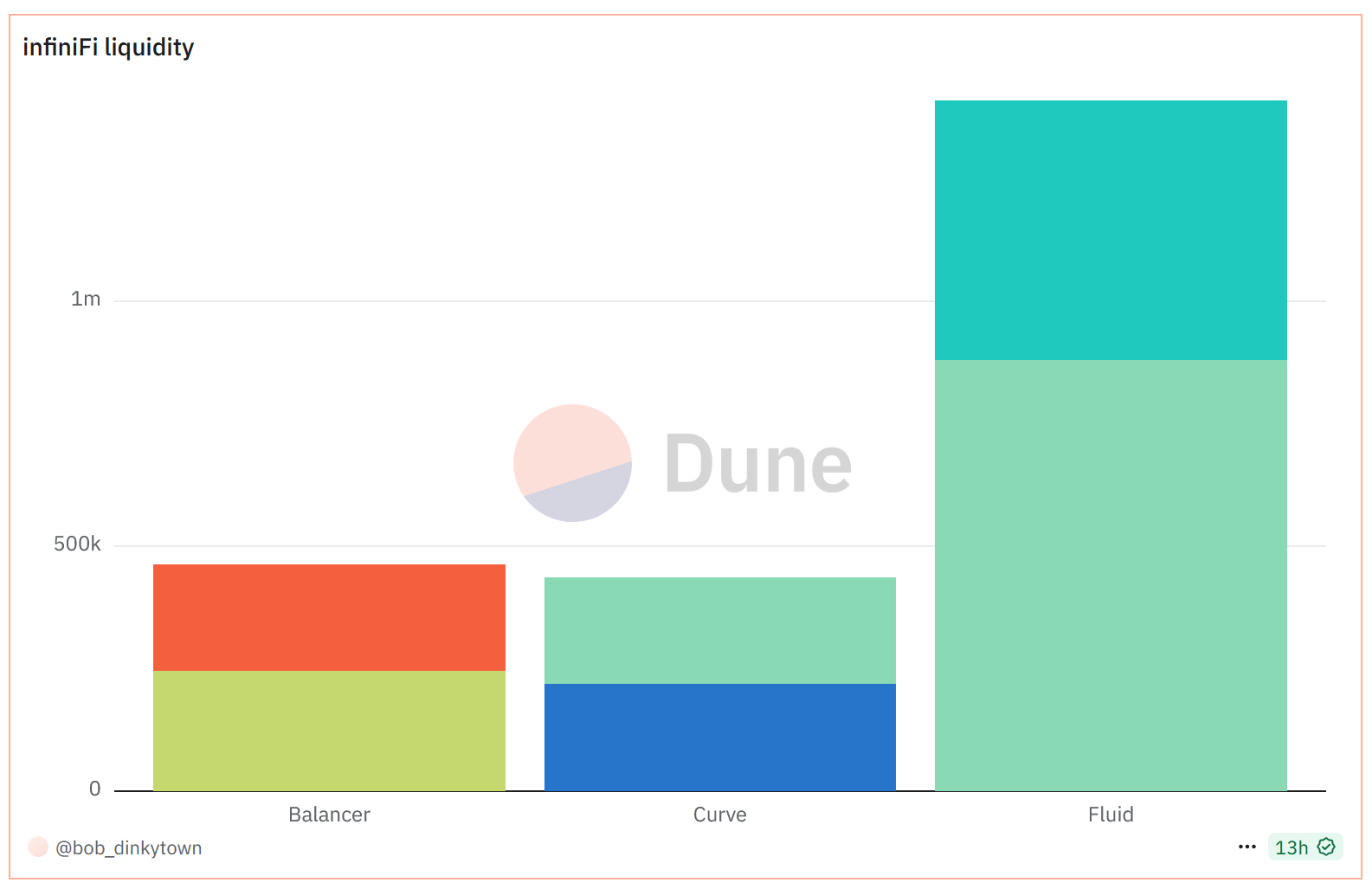

InfiniFi’s reserve composition is completely transparent onchain, so you don’t have to rely on a quarterly call report.

You can easily look up USDC deposits and iUSD tokens minted against it to determine its exact asset-liability mismatch, if any.

You can also examine a breakdown of the protocol’s yield strategies, or whether the protocol is abiding by its liquidity buffers — down to the amount and type of assets they’re made up of.

Source: Dune.

Source: Dune.

In the event of a hack or “bank run,” an explicitly coded loss waterfall will determine who gets paid in order.

The highest-yield and locked liUSD token holders are first in the firing line, absorbing losses first.

[ad_2]