This is a segment from the Forward Guidance newsletter. To read full editions, subscribe.

It’s clear at this point that one of the Trump administration’s primary goals is to lower trade deficits with other countries, specifically goods trade deficits.

Source: Fred

It’s important to make that distinction because, in fact, the US runs a services surplus!

The US mechanically imports “stuff” from other countries that manufacture it both better and cheaper. And as the reserve currency of the world, US dollars flow into those other countries to fund those purchases.

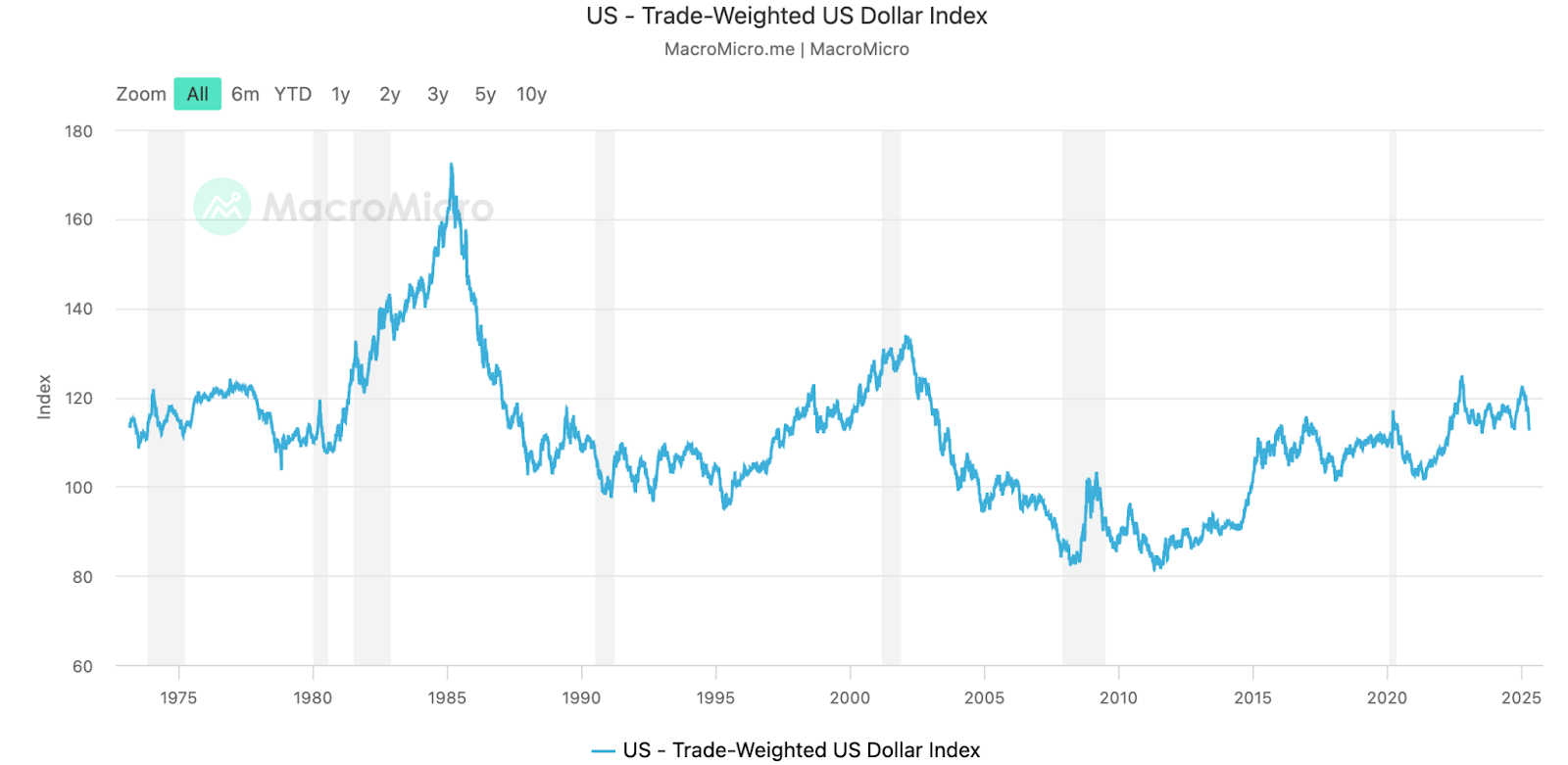

Those foreign dollars then get reinvested and held in US-denominated assets such as Treasurys and US equities. This mechanical demand has created an artificially strong US dollar for many decades, paired with a hollowing out of the US middle class whose manufacturing jobs have been offshored.

Source: MacroMicro

Effectively, the grand tradeoff in globalism has been access to cheap “stuff” but a hollowing-out of that once-strong manufacturing base.

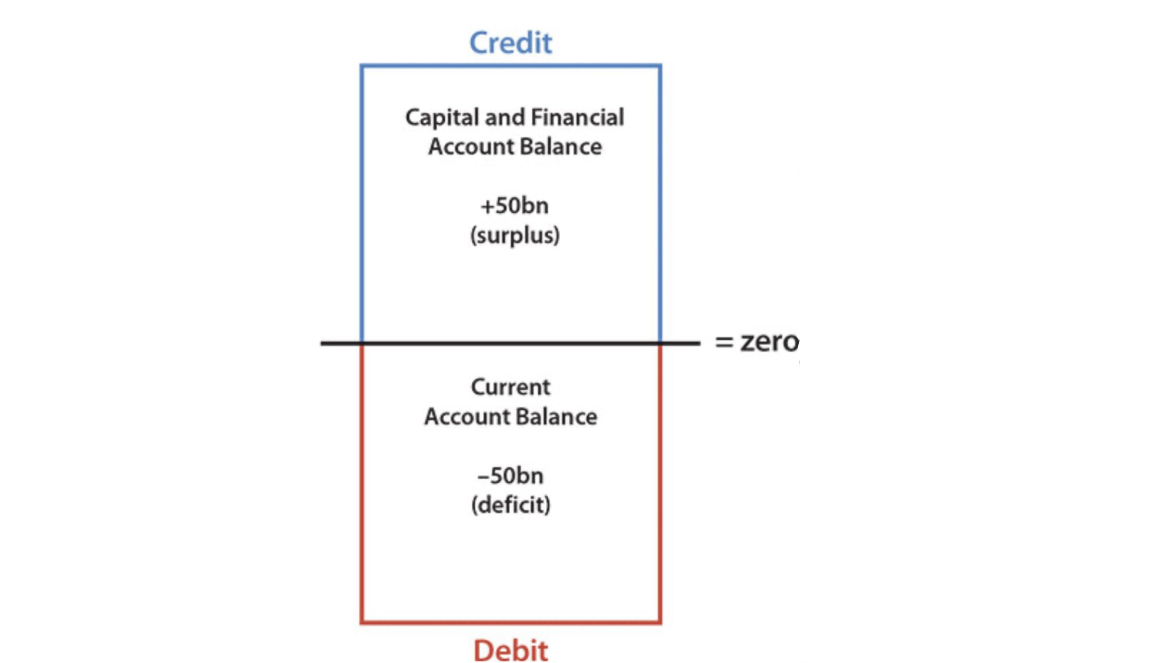

One of the great laws of (economic) nature is the balance of payments equilibrium. Mechanically, that currency account deficit (stuff coming in) must be offset by a capital account surplus (money going out to pay for the stuff coming in).

This structural capital account surplus that’s held for many years has resulted in a structural bid to US denominated assets. That has led to mechanically-lower Treasury yields (lowering borrowing costs for the government) and higher multiples on US equities relative to other countries (a P much greater than E, in a typical P/E ratio).

The Trump administration has been loud and clear that it wants to decrease the current account deficit. Although it doesn’t speak this second part as loudly, that comes with a lower capital account surplus that would reverse that trend of lower bond yields and higher equity multiples. Effectively, the Trump administration is telling foreigners to take their money and bring it home.

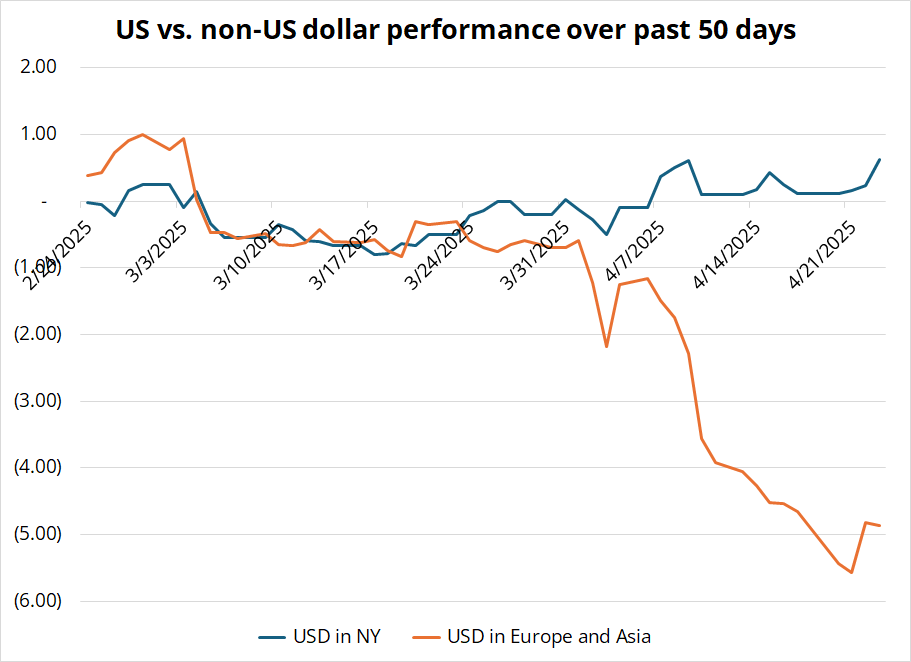

Foreigners aren’t wasting any time getting to work. This chart from Brent Donnelly showcases how all the action in selling those US-denominated assets is happening during the market sessions of those foreign countries. During the NY session, US dollar performance remains steady. However, during the Europe and Asia sessions, it’s a race for the exits.

Source: Brent Donnelly

It is rational for foreign asset managers to exit these assets if the capital account premium baked into US assets is being questioned. It would lead to higher bond yields and lower equity prices.

Effectively, the world needs to reprice the US Treasury yield that is the bedrock of nearly all global relative valuations with a risk premium in it. My terrible attempt at Photoshop (I’m a trader, not a designer, okay?) showcases this mechanic below:

It remains to be seen how durable this unwind of the current account deficit will be, but by all accounts, it means one thing: Get out of US-denominated assets.

The president of the United States is basically telling you to.